However they dress up the rhetoric, economic orthodoxy is convincing too many politicians of all parties that there is no choice but to accept austerity economics. They should know better, as a number of commentators are pointing out.

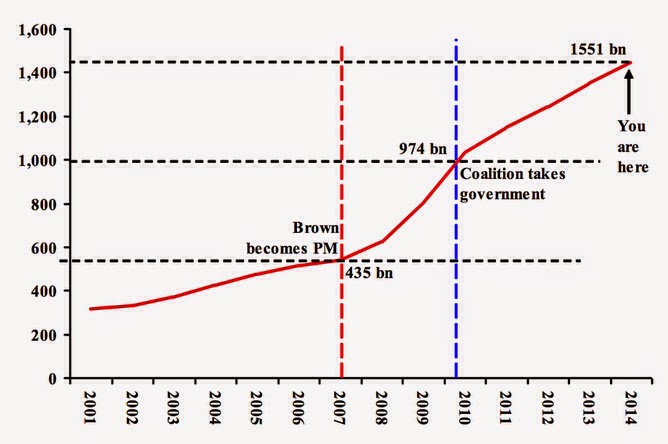

Professor John Weeks from University of London has provided an excellent economic history lesson to explain why austerity doesn't add up. When Osborne became chancellor the UK public debt was £974 billion (63% of GDP), and at the end of this September, four years and five months later, the debt was £1451 billion (80% of GDP). This increase of £475 billion exceeded the so-called ballooning of debt under Gordon Brown that, through a massive recession, rose by £440 billion.

In fact Osborne has put on more debt during his years of "sound fiscal policy" and much-touted recovery that Brown did during an economic collapse. In contrast Gordon Brown's fiscal stimulus stopped the rise in public borrowing in late 2009. Increased spending stopped borrowing from rising, because that spending arrested the fall in the economy that had created the need for more borrowing. In contrast Osborne has been incapable of bringing borrowing down. This is because his expenditure cuts undermine growth. Slow growth means slow revenue recovery, hardly rocket science even for Osborne.

Steve Keen from Kingston University warns that we are heading for another financial crisis, but not for the global economic reasons Cameron is using as his latest excuse. Cameron is panicking about a rising level of government debt, when at 91% of GDP, it’s 80 percentage points below the level of private debt. If Cameron thinks reducing government spending when private credit is contracting is good economic policy, then he’s ignoring the biggest car crash in economic history – the European Union, where government austerity turned the crisis into a second Great Depression.

Martin Wolf in the Financial Times (£) also questions Cameron's concerns about the global economy. He points to the difficulties caused by the fiscal austerity that his government recommends have become particularly evident in Japan and the eurozone. He argues that these stagnant high-income economies are the weakest links in the world economy. To understand why, he says we need to analyse today’s most important economic illness: chronic demand deficiency syndrome.

He points to three reasons for this. Firstly the post-crisis overhang of private debt and the damage to confidence caused by the sudden disintegration of the financial system. Secondly, and almost the opposite, economies suffer not just from a post-crisis balance-sheet recession, but from an inability to generate credit-driven demand on the pre-crisis scale. Thirdly, slowdown in potential growth, due to some combination of demographic changes, slowing rises in productivity and weak investment. But he says that this last set of explanations feeds directly into the second. If growth of potential supply is expected to slow, consumption and investment will be weak. That will generate feeble growth in demand.

Of course Osborne is less concerned about the effectiveness of austerity economics, than his long term plan to reduce the role of the state. Austerity is just an excuse for his ideological goals. What is more worrying, as John Weeks points out, is Ed Ball's conversion to austerity. Is it that the political strategy of being fiscally tough outweighs economic common sense? What he should do is go back and read his own Bloomberg lectures. I once told him that I thought he understood economics then, but it's not too late to change course and adopt a different more progressive political and economic strategy.

No comments:

Post a Comment